Fed Raises Interest Rates for the 7th time

The Fed raises rates for the 7th time

I listened to our new Fed chairman, Jerome Powell, on June 13th, 2018. It was refreshing to hear the new Fed chairman speak in actual plain English. His predecessors, both feds and economists, were so longwinded with so many disclaimers, by the time they got to the meat of the program; most people had already changed the channel.

Why should you care?

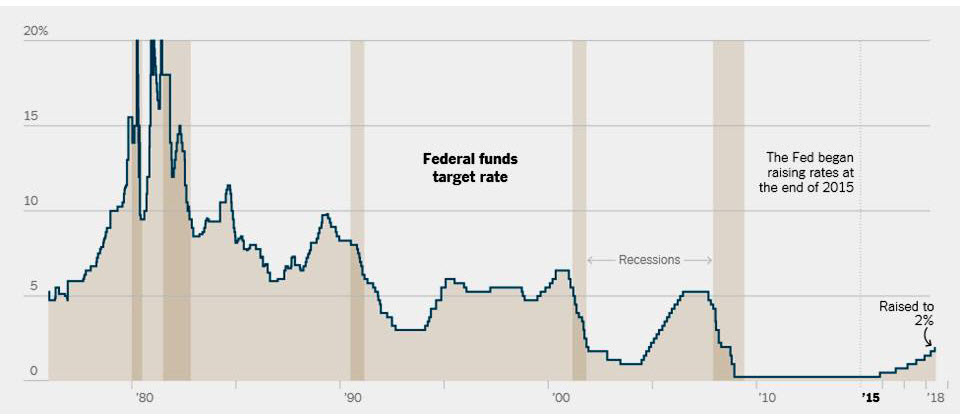

Well, you should probably care if you have a credit card, auto loan, mortgage, more than $10,000.00 in a Money Market CD or you own a bond. You should definitely care if you’re an investor Many advisors like myself believe that the Fed, through higher rate, actually end up causing recessions which the precursor to recessions is normally the market’s meltdown. Do you remember the years 2000-2002 and 2008-2009? I want you to take a look at this chart.

Note: Rate is the federal funds rate until Sept. 27, 1982, the federal funds target rate until Dec. 15, 2008, and thereafter it is the upper limit of the federal funds target rate range. | Source: Federal Reserve <1>

<1> https://www.nytimes.com/interactive/2018/business/economy/fed-rates-powell.html

Focus on the chart around 2005, 2006, 2007 and 2008. The Fed raised rates and then poof, in 2008, the economy melted down. Therefore, we had a big recession. Can you remember back to the late 1990’s when the economy was doing great? From 1997-1999 the Fed raised rates to cool things down. Do you remember the last recession we had with the accompanying bear market? A lot of people have even forgotten about that recession that was caused in 1990.

Do you see where the Fed was raising rates before that? And it makes sense if you think about that. For example, let’s say you have a 4% mortgage today and the Fed raises rates to where the mortgage rate goes up to an equivalency of 6% – 7%. How many people do you know who’re going to go buy a new home and pay many thousands of dollars more per year on interest payments? I can guarantee you probably not too many. How many people do you know that would go from a 7% auto loan to a 10% or 11%? Not many if any. So, this is how the Fed tries to manage the economy.

Now remember, their mandate is just two things: to try to keep inflation around the 2% level and full employment. Their mandate is not to drive up the stock market. The good news is the tide is still coming in, but maybe we need to start repositioning the boat in deeper water so we’re not stranded when the tide starts going out (recessions).

Sincerely,

John Romano, CFP®

====================================

Footnote:

<1> https://www.nytimes.com/interactive/2018/business/economy/fed-rates-powell.html

John Romano, CERTIFIED FINANCIAL PLANNER™, has over 30 years experience in the financial field. John is a Registered Representative with Securities America, Inc. (member of the FINRA and SIPC), and an Investment Advisor Representative with Securities America Advisors. He has prepared hundreds of reports for retirees to assist in their retirement income planning needs. He is dedicated to providing portfolio analysis, dividend and income information, and investment management services to retirees (and those preparing to retire) in The Villages, Florida, and has clients throughout the United States.

The opinions and forecasts expressed are those of the author, and may not actually come to pass. This information is subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any specific security or investment plan. Past performance does not guarantee future results.

Securities offered through Securities America, Inc. Member FINRA/SIPC, John Romano CFP® Registered Representative. Advisory Services offered through Securities America Advisors, Inc. John Romano Investment Advisor Representative. Romano Income Strategies and Securities America are not affiliated.

Trading instructions sent via e-mail may not be honored. Please contact my office at (352)753-8590 or Securities America, Inc. at (800) 747-6111 for all buy/sell orders. Please be advised that communications regarding trades in your account are for informational purposes only. You should continue to rely on confirmations and statements received from the custodian(s) of your assets. The text of this communication is confidential and use by any person who is not the intended recipient is prohibited. Any person who receives this communication in error is requested to immediately destroy the text of this communication without copying or further dissemination. Your cooperation is appreciated.

305 Skyline Drive, Suite 3, Lady Lake, FL 32159

Phone: 352-753-8590

Email: John@RomanoJohn.com